Appendix D. A quick reference on key financial AI metrics

In academic machine learning, metrics are abstract mathematical optimizations. In financial AI, metrics are money. A model with 99% accuracy might still bankrupt a lending portfolio if it fails to rank-order risk correctly, and a high-precision fraud model might cause millions in lost revenue if it creates unacceptable friction for VIP customers.

This appendix provides a comprehensive reference to the advanced metrics used across the four major domains of this book. It details the exact calculation methods alongside their business translation and strategic trade-offs.

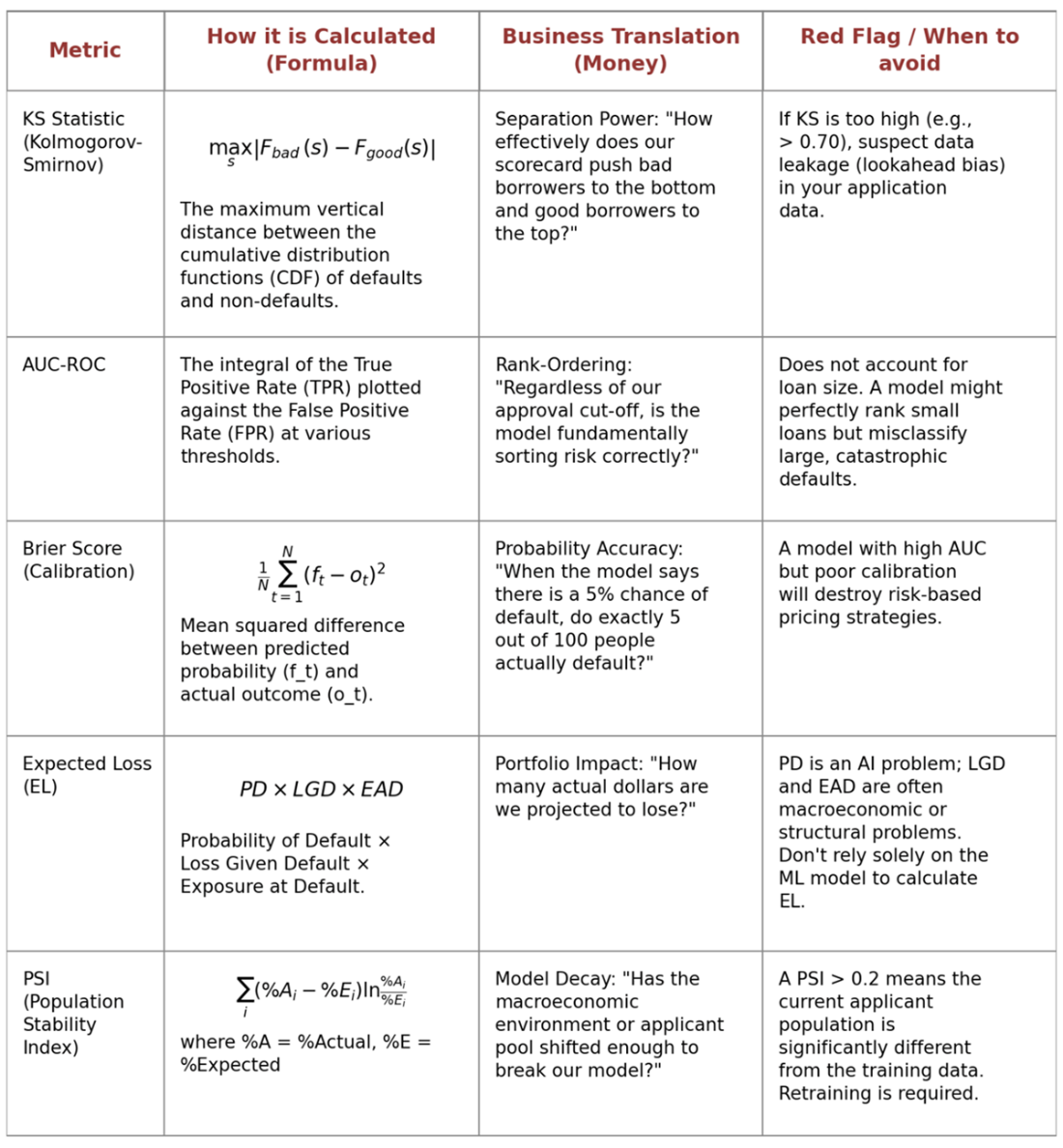

D.1 Credit risk and stability metrics (Part 2)

Credit models are evaluated on their ability to cleanly separate "good" from "bad" borrowers across a probability continuum, their calibration to true default rates, and their stability over time.

Table D.1 Core metrics for credit scoring

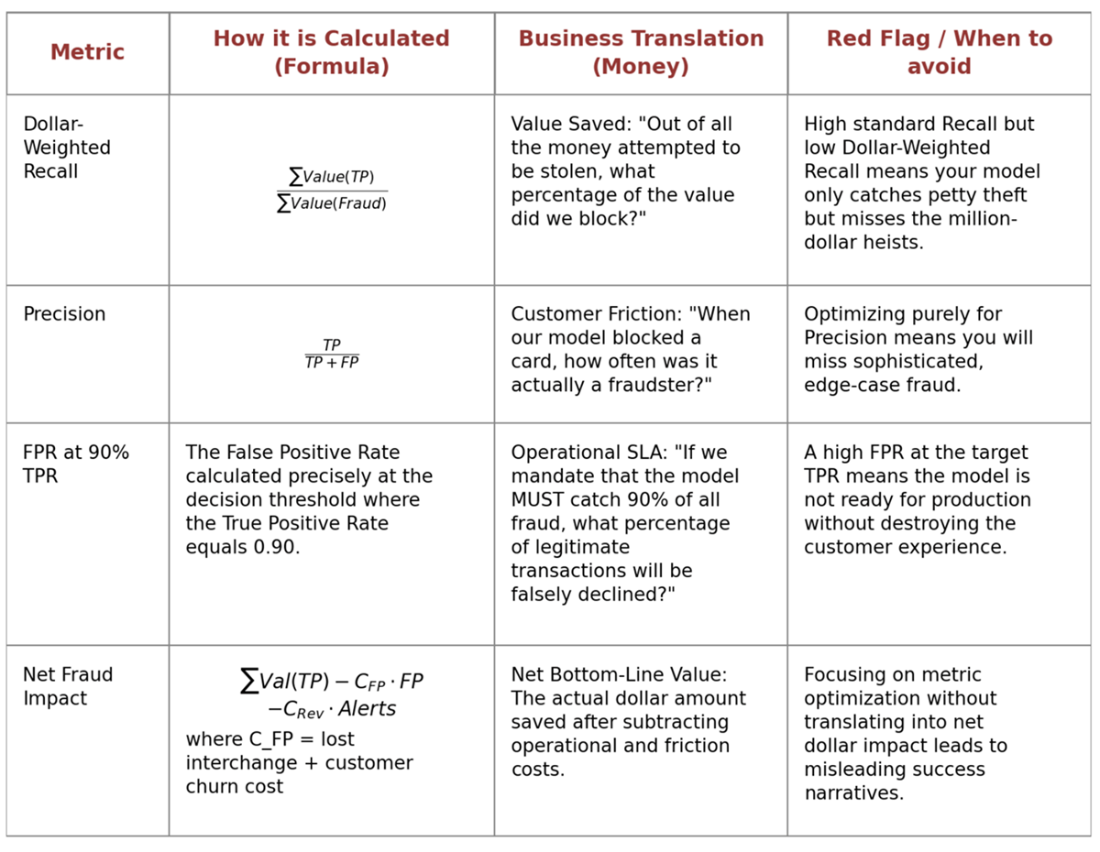

D.2 Fraud and imbalanced classification metrics (Part 3)

Financial fraud datasets are notoriously imbalanced. Furthermore, fraud must be evaluated not just by the count of transactions, but by the monetary value and the holistic cost of operations.

Table D.2 Core metrics for fraud detection

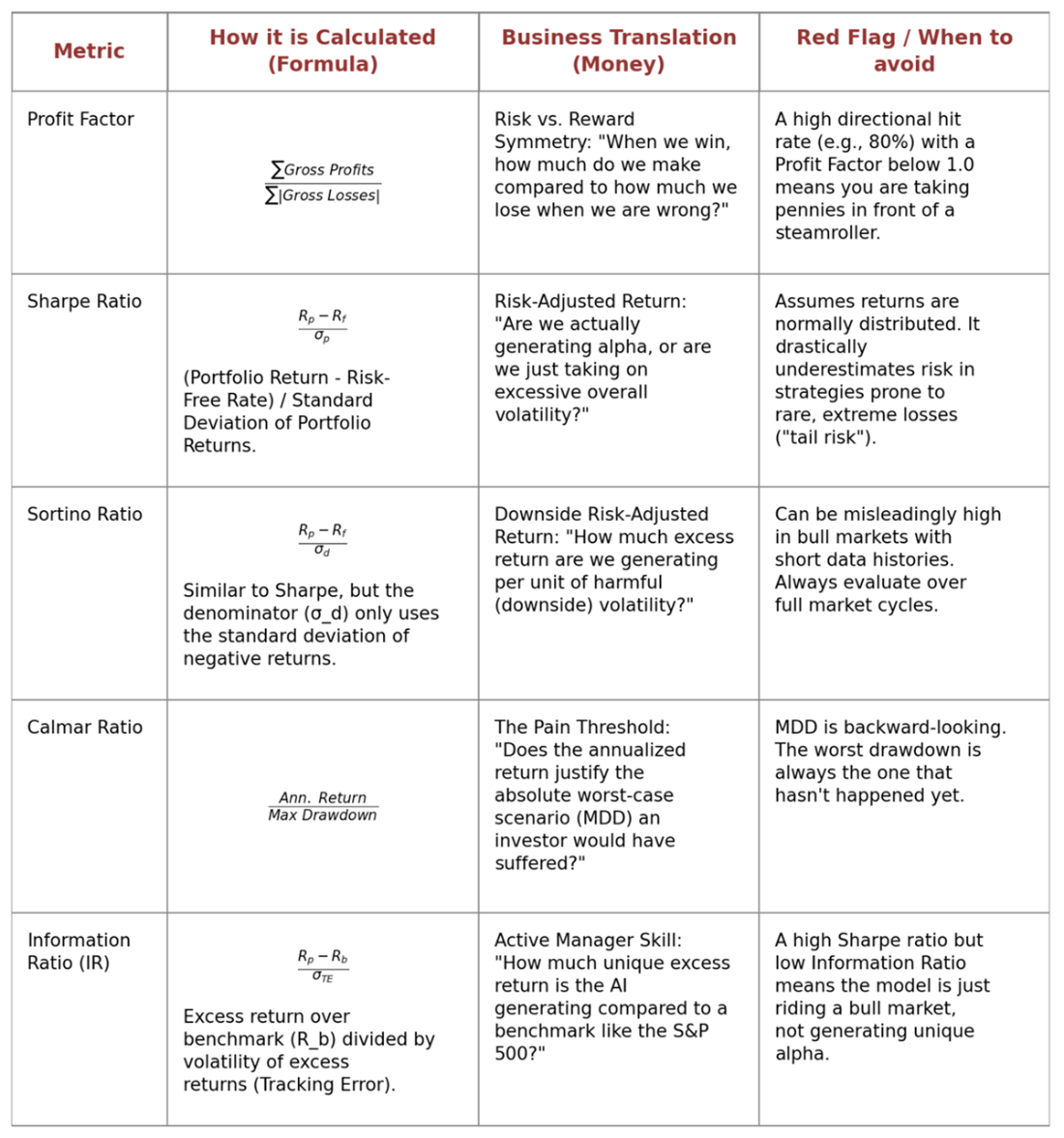

D.3 Investment and market prediction metrics (Part 4)

Evaluating risk in quantitative trading requires looking beyond normal distributions. It is vital to measure the symmetry of payoffs and the penalty for downside volatility.

Table D.3 Core metrics for quantitative investing